Copper Mining Stocks and Gold Mining Stocks: Why a Middle East Ceasefire Favors Both

If a Middle East ceasefire restores Hormuz logistics and cools energy prices, copper mining stocks look like the highest-upside recovery trade, with gold mining stocks close behind.

If the Middle East ceasefire holds and shipping through the Strait of Hormuz normalizes, the cleanest mining trade is not aluminum. It is not coal. It is copper mining stocks first, then gold mining stocks.

That is the real signal inside the Daniel Major note summarized in the brief. The market spent the conflict phase rewarding whatever benefited most directly from disrupted energy logistics and panic pricing. A ceasefire changes the ranking. Once oil and gas stop acting like the dominant macro variable, investors can go back to asking a more useful question: which mining equities still have structural demand behind them, but have already been punished as if the demand story broke?

StackFi’s answer is straightforward. Copper miners offer the best risk/reward in a cooling-energy scenario because the demand story remains intact while supply stays constrained. Gold miners come next because gold can stay structurally expensive even if the war premium fades. The implication is important: a ceasefire is not automatically bearish for gold-related equities. It can actually improve the setup for high-margin gold producers by lowering cost pressure without necessarily breaking the gold price regime.

Why a ceasefire helps copper mining stocks the most

The copper case starts with a simple market mismatch. Copper equities sold off as if a prolonged energy shock would choke industrial demand and flatten the growth outlook. But if the ceasefire makes Hormuz traffic workable again and drags oil lower, that specific demand-kill mechanism weakens fast.

According to the UBS summary in the brief, COPEX and the broader copper-miner complex had fallen roughly 20% since the conflict began. That drawdown matters because it happened while one of the most important bullish facts in copper never changed: the world still does not have enough easy new supply.

The clearest example is Ivanhoe Mines’ Kamoa-Kakula complex, where 2026 and 2027 output expectations were cut again by roughly 100 ktpa. That is not a tiny miss. It is another reminder that large, high-quality copper projects remain vulnerable to operational setbacks, political friction, and execution risk even when long-term demand is obvious.

StackFi’s read is that the market briefly priced copper like a cyclical victim of war. A ceasefire lets investors re-rate it back toward what it actually is: a structurally scarce input into electrification, grid upgrades, AI infrastructure, and industrial re-shoring.

Why copper’s demand story still looks stronger than the tape

The bullish copper thesis is not just “China might stabilize.” It is broader and more durable than that.

Renewable buildout, transmission investment, power equipment demand, and manufacturing relocation all still point to higher copper intensity over time. In fact, an energy shock can strengthen part of that thesis, because expensive and unstable fossil-fuel logistics tend to reinforce policy and corporate spending on electrification and domestic resilience.

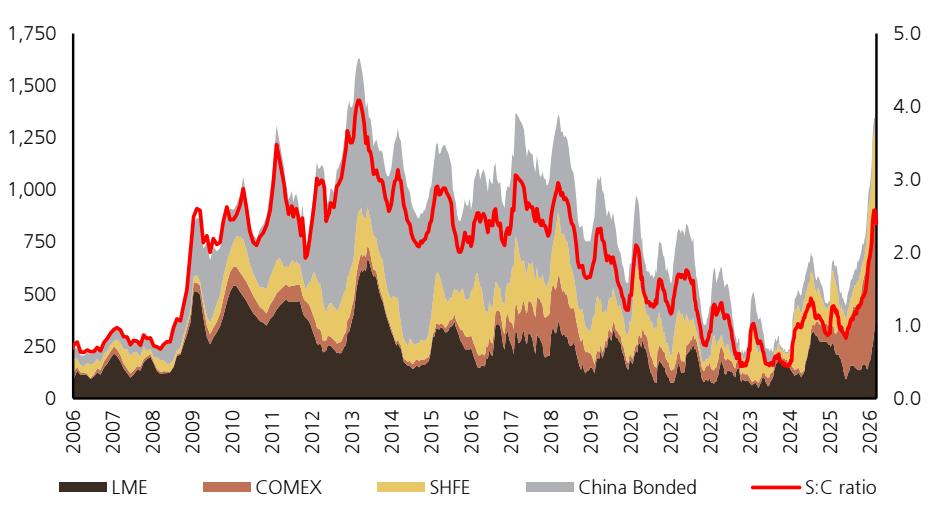

The inventory picture in your supplied chart helps explain why this matters. Visible copper inventories across LME, COMEX, SHFE, and bonded China warehouses have risen from the lows, but the stock-to-consumption ratio has also rebounded sharply in 2026 rather than collapsing demand outright. That is not the picture of a dead market. It is the picture of a market that remains globally tight enough for inventory composition and drawdowns to matter.

Visible inventories have risen, but the stock-to-consumption ratio has also turned sharply higher in 2026. For StackFi, the important point is not just the headline stockpile. It is whether a post-ceasefire recovery allows the market to re-focus on copper’s still-constrained supply path.

The UBS note also highlights that while global visible inventories approached 1 million tonnes, Chinese stocks had already begun to decline seasonally. That split is important. Western macro traders can dump copper on recession fear, but if Chinese physical demand is drawing inventory in line with seasonal norms, the physical market can reassert itself quickly.

That is why we think Freeport, First Quantum, and the Anglo/Teck complex fit the post-ceasefire setup better than the market currently prices. The point is not that all risks vanish. The point is that the valuation reset looks too severe for a metal whose supply side remains this constrained.

Why gold mining stocks still work even if the war premium cools

A lot of investors make the same mistake whenever geopolitical stress starts to fade: they assume lower war premium automatically means lower gold and therefore weaker gold miners. That is too simplistic.

The better way to think about gold in this setup is to separate transient geopolitical premium from structural monetary support.

If oil rolls over and the ceasefire reduces near-term inflation pressure, that can actually help gold in one important way: it reduces the risk that central banks are forced into a harsher, longer-lasting energy-driven inflation regime. That matters because the bigger drivers behind the gold bull cycle were never just missiles and tanker routes. They were already in place:

- fiat debasement concerns

- diversification away from US asset concentration

- reserve managers increasing non-dollar exposure

- private investors looking for a more credible hard-asset hedge

That is why the UBS summary can stay constructive on gold miners even in a cooling scenario. If gold stays anywhere near the $4,000/oz zone and large-cap producers are still running AISC below $2,000/oz, the cash margins remain exceptional.

For StackFi, that is the real equity point: a ceasefire can take pressure off miners’ input costs without necessarily destroying the gold price floor. In other words, the macro can become less chaotic while gold mining economics remain very attractive.

Why aluminum and coal look more like give-back trades

The relative losers in a de-escalation scenario are the assets whose outperformance depended most directly on disruption staying severe.

The UBS summary notes that LME aluminum rose 10% during the conflict and outperformed copper by roughly 15%, largely because around 3 million tonnes of Middle East smelting capacity were damaged or disrupted. When you add the reported issues around EGA Al Taweelah and damage at ALBA, the price response makes sense. The market was paying for real outage risk.

But that is exactly why aluminum looks less attractive if the region cools down. The trade was too dependent on stress staying acute.

The same logic applies to thermal coal and related high-energy-cost beneficiaries. Their relative strength came from a world where expensive oil and gas created scarcity rent. If shipping normalizes and energy prices back off, those scarcity rents should compress.

This is the core ranking shift:

- conflict escalation favored energy shock beneficiaries

- ceasefire favors structurally scarce metals with better long-run demand

That is why copper miners move to the front of the queue, while gold miners remain attractive because their macro support is broader than just war premium.

The missing nuance: a ceasefire can stabilize markets and still weaken dollar credibility

This is where StackFi’s view diverges from the shallow “risk-on means gold down” take.

Yes, a ceasefire can produce a relief rally in broad equities, including AI leadership names. Yes, it can calm markets temporarily. But it does not erase what the episode revealed about the global system. If another major energy and shipping shock can so quickly threaten inflation, logistics, and sovereign confidence, then the long-term credibility of the dollar-centered system does not come out stronger. It comes out more contested.

That is one reason we are cautious about both extremes in gold discourse. We do not think a ceasefire means the gold bull market is over. But we also do not think “$10,000 gold is inevitable” is a serious base case under current demand assumptions.

At today’s structure, central banks are still the most dependable support bid for gold, and that flow is relatively steady rather than explosive. Under a continuation of current supply-demand dynamics, a level more like $7,000 looks easier to argue as a stretched ceiling than an immediate move to five digits. To get something dramatically above that, the market would probably need a different buyer mix: financial institutions and private investors accumulating gold at scale, not just central banks grinding higher month after month.

That nuance matters for gold mining stocks. You do not need fantasy gold prices for the equities to work. You just need gold to stay high enough, long enough, for margins and free cash flow to stay exceptional.

How we would rank the mining opportunity set now

If the ceasefire proves durable, this is the StackFi ranking:

- Copper mining stocks

- Gold mining stocks

- Royalty / streaming names

- Aluminum and coal laggards after relative outperformance

Copper sits first because it combines the best cyclical rebound potential with the strongest structural scarcity story. Gold miners come second because their economics still look excellent, but their upside is less about growth recovery and more about preserving a high gold regime with lower cost pressure. Royalty names such as Wheaton and Franco-Nevada remain attractive if you want gold exposure with less operating-cost risk.

The stock-specific names in the UBS summary fit that ranking well:

- First Quantum for a restart catalyst at Cobre Panama

- Freeport for valuation discount plus Grasberg normalization

- Anglo and Teck for quality copper exposure and strategic optionality

- Newmont, Endeavour, SSR, and Skeena on the gold side

- Wheaton and Franco-Nevada for cleaner margin profiles

The big takeaway is that the best post-ceasefire setup is not “buy whatever went up during the war.” It is buy what sold off even though the long-term case still improved.

If you want to connect this setup back to the broader commodity rotation, continue with JPM Commodity Flows: Energy Bleeds $33B, But Smart Money Loads Crude, Gold and Silver Volatility 2026: What Energy Shock Signals, and How to Invest in Gold in 2026. If your next question is how to own gold itself rather than the miners, start with Physical Gold vs Gold ETF vs Tokenized Gold.

FAQ

Why do copper mining stocks benefit from a Middle East ceasefire?

Copper mining stocks benefit because a ceasefire reduces the risk that an energy shock crushes industrial demand. Once oil and shipping stress cool, investors can refocus on copper’s tighter long-term supply picture and resilient demand from electrification, grids, and infrastructure.

Are gold mining stocks still attractive if the war premium fades?

Yes. Gold mining stocks can still work if the war premium fades because gold’s support does not come only from geopolitics. Reserve diversification, monetary distrust, and high spot prices versus sub-$2,000 AISC can keep miners highly profitable even in a calmer geopolitical environment.

Why are aluminum and coal less attractive in the cooling scenario?

Their relative outperformance was more dependent on disruption staying severe. If Middle East logistics normalize and energy prices fall, the scarcity premium supporting aluminum and coal should compress faster than the structural case behind copper and gold miners.

What is the key risk to the bullish copper-miner thesis?

The biggest risk is that the ceasefire does not hold or that global growth weakens enough to overwhelm the supply-side story. Copper miners are still equities, so they can sell off hard if the market moves from energy fear into outright recession fear.

Does a ceasefire kill the long-term bull case for gold?

No. A ceasefire can remove some short-term geopolitical premium without reversing the deeper reasons investors and central banks still want gold. What it may change is the pace of the move, not necessarily the direction of the longer cycle.